Financial statements for small business owners are essential tools for evaluating your company's financial health, securing funding, and making informed strategic decisions.

There are three primary financial statements every small business owner should understand:

- Balance Sheet

- Income Statement (also known as Profit & Loss or P&L)

- Cash Flow Statement

Together, these form what's commonly referred to as the “three-statement model.”

These three financial statements for small business provide clarity on your company's performance, highlighting strengths, revealing risks, and pinpointing opportunities for improvement. Critically, they enable you to effectively communicate financial health to potential investors, lenders, and other stakeholders.

Below, we will go into an introduction to each of these three financial statements, exploring how they are important tools that can help provide a dashboard into your company's financial health.

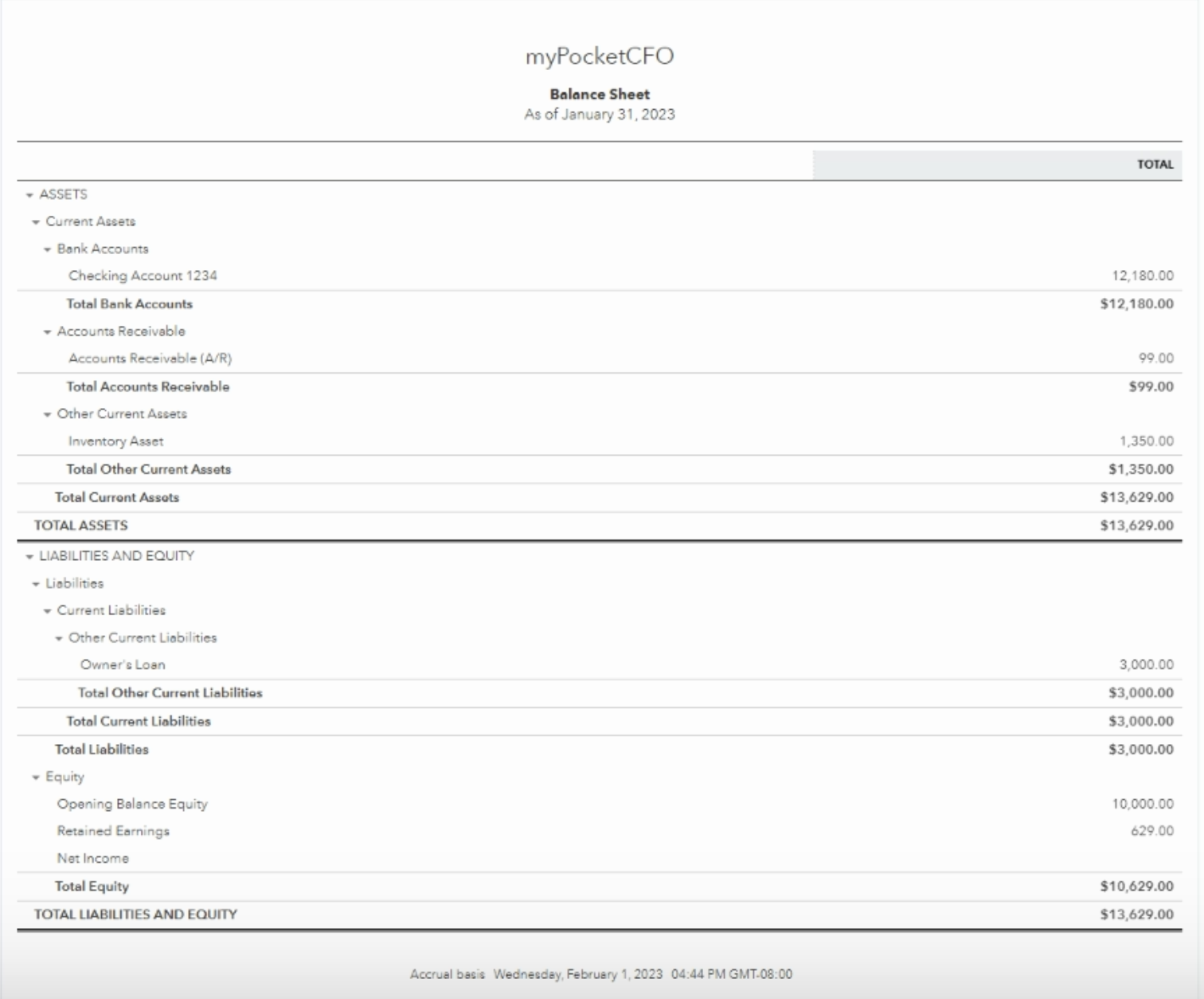

Statement 1: Balance Sheet

The balance sheet provides a snapshot of your business's financial standing at a specific point in time. It shows your company's assets, liabilities, and equity:

Assets = Liabilities + Shareholder’s Equity

This equation represents the "balance" in the Balance Sheet. Assets (cash, inventory, receivables, equipment) hold debit balances, while liabilities (payables, payroll, credit card balances, loans) and equity (owner contributions, retained earnings) carry credit balances.

The Balance Sheet categorizes assets and liabilities into:

The Balance Sheet Drives Important Ratios for Small Businesses

Key ratios derived from the balance sheet help small businesses assess financial stability:

Current ratio

A current ratio greater than 1 suggests your business can comfortably meet short-term obligations. A ratio below 1 indicates a need for additional cash, potentially from owner contributions, external investments, or new debt arrangements.

Other ratios

Other crucial ratios include:

Higher ratios indicate more reliance on debt, implying greater financial risk. Investors closely evaluate these ratios to determine the sustainability of small businesses.

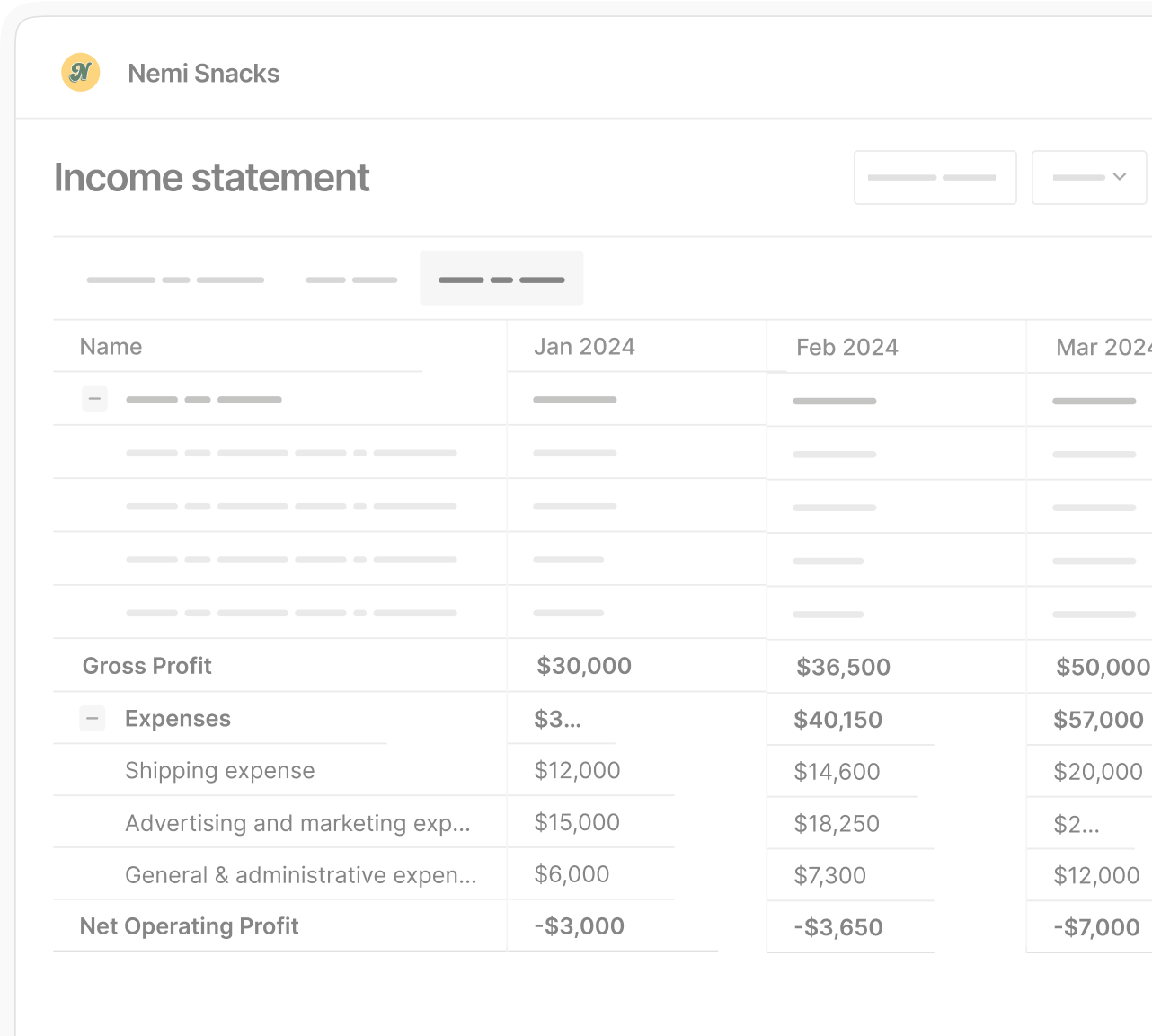

Statement 2: Income Statement

The Income Statement details your small business's revenue and expenses over a period — monthly, quarterly, or annually. It breaks costs into direct (Cost of Goods Sold) and indirect expenses (overhead). The result after subtracting all costs from revenue is your Net Income, or bottom line.

Gross margin

A critical metric from the Income Statement is Gross Margin:

Gross Margin = Revenue – Cost of Goods Sold

Improving gross margin is crucial for small businesses looking to boost profitability and attract investors.

Asset Turnover Ratio

Another key measure:

This indicates how efficiently your business uses assets to generate sales. A ratio of 1 means you are generating $1 in sales per dollar invested.

Statement 3: Statement of Cash Flows

The Cash Flow Statement shows how cash moves in and out of your business through operating, investing, and financing activities:

-

Operating Activities: Daily receipts and payments (vendors, customers, payroll).

-

Investing Activities: Purchases or sales of assets (equipment, property).

-

Financing Activities: Loans, investments, and debt repayments.

For small businesses, the cash flow statement highlights liquidity and identifies potential cash shortfalls before they become critical issues.

FAQ: Financial Statements for Small Business Owners

-

Why do small businesses need financial statements? Financial statements help you manage cash flow, make strategic decisions, attract investors, and meet regulatory requirements.

-

How often should financial statements be prepared? Monthly statements are a minimum, but with modern tools, statements can be updated weekly, and sometimes even more frequently, to provide insights.

-

Can I create financial statements on an ongoing basis? Yes, and accuracy and timeliness are critical. Partnering with advisors and using reliable software is highly recommended.

Understanding financial statements for small business owners is critical for founders — they aren't just for finance professionals. Accurate, clear, and timely financial statements empower better decision-making, ensure business sustainability, and provide essential insights to potential investors, lenders, and partners.

Financial statement literacy is critical to set your small business up for long-term success.